Q&A on the Gulf-Africa investment corridor with Simon Quijano-Evans

The Gulf-Africa investment corridor is becoming increasingly established and strategically relevant, driven by shared priorities around energy transition, food security, infrastructure and economic diversification. Capital flows are increasingly disciplined, with Gulf investors placing greater emphasis on long-term partnerships, scale and credible execution. This evolving dynamic comes against the backdrop of heightened regional tensions following the Iran conflict and the UAE’s decision to exit OPEC, a move that underscores a shift toward greater strategic autonomy.

In our Q&A, Simon Quijano-Evans draws on decades of experience as Chief Economist for banks and investment funds, assessing frontier and emerging markets to reflect on how the corridor has evolved and where it is heading. His perspective highlights a desirable shift for African corporates – moving beyond viewing the Gulf as a source of capital, and instead presenting clear, transparent and strategically aligned investment propositions.

1. You have been tracking frontier and emerging markets for decades – how would you characterise the evolution of the Gulf–Africa investment corridor over the past 10–15 years?

Gulf–Africa economic engagement has grown steadily over the past decade, with foreign direct investment largely flowing from GCC countries into Africa, while trade has developed as a more reciprocal, two-way relationship.

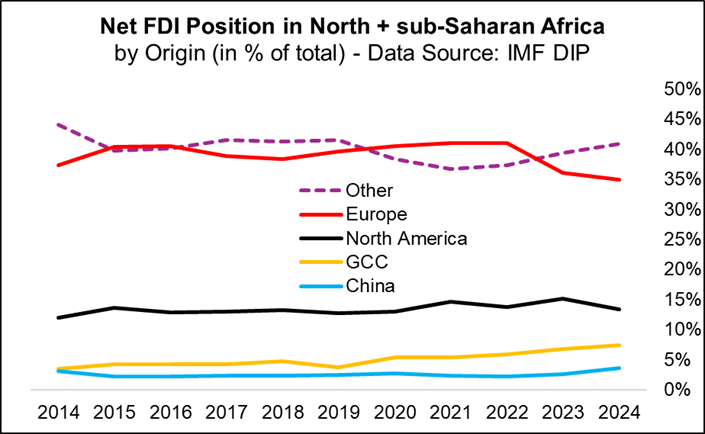

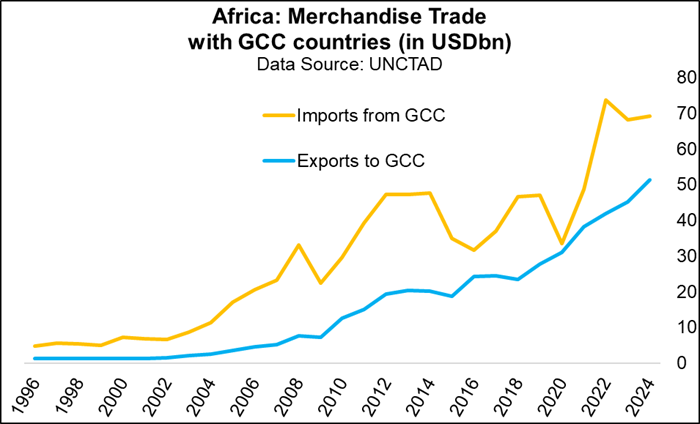

According to the IMF’s DIP data, GCC countries’ net Foreign Direct Investment position (or FDI stock) in North and sub-Saharan Africa doubled between 2014 and 2024 to reach almost 8% of the world’s total FDI stock in Africa (Figure 1). While Africa has traditionally faced a trade deficit with the GCC, total exports + imports between GCC and Africa have doubled over the same time-frame to USD 120bn, according to UNCTAD data (Figure 2).

2. What has fundamentally changed in the nature and expectations of capital flowing between the Gulf and Africa – are we now seeing a shift toward more strategic, long-term, and institutionally driven investment?

The Gulf and Africa are both at a pivotal moment when it comes to long-term strategic investment decisions. The global shift in energy usage poses transformational challenges for most hydrocarbon-exporting economies. At the same time, the Gulf and much of Africa need to continue addressing the need for sustainable food and water security. A deepening of collaboration in these areas comes with greater engagement and planning in trade and logistics.

3. Which sectors are emerging as the most compelling for Gulf investors in Africa, and where do you see the strongest alignment between capital and credible, scalable business models?

Renewable energy, critical minerals, food production, livestock, the financial industry and tourism are all plausible areas for Gulf investors to continue focusing on in Africa, given the mutual benefits of further developments in these sectors. Saudi Arabia, for example, has substantial know-how in green hydrogen, as seen in its sizeable investments in Egypt. Kenya, on the other hand, will need to find ways to store and export excess renewable electricity in the coming years, opening the way to collaboration on the green hydrogen front. A number of GCC countries have already invested into large areas of land in east Africa for agricultural purposes, while GCC airlines and UAE port operators have increased their footprint around Africa in recent years.

4. How should African corporates think about the Gulf beyond a source of capital – particularly in terms of long-term partnerships, market access, and operational scaling?

In recent years, the world has often looked to the Gulf solely as a provider of capital. African corporates would do well in seeking counterparties in the Gulf that can see themselves as partners rather than only one-way providers of funds. African entrepreneurs should also be pro-active in identifying areas where both sides can be mutual beneficiaries, including in the areas of alternative energy and food and water security. This could include some commitment of African capital for investments into GCC.

5. As competition for capital intensifies, what distinguishes businesses that successfully attract Gulf investors – in terms of governance, strategic clarity, and overall credibility?

Today, Gulf investors are highly sophisticated and will want to see all those criteria addressed in potential investment projects, especially as the competition for their capital is intense. African corporates could also look to establishing cross-country joint ventures within Africa to provide foreign investors with more scale and diversification opportunities.

6. To what extent does a clearly articulated equity story or investment narrative influence outcomes, especially in markets where investor perception of risk can be a barrier?

It is undeniable that foreign investors face extensive due diligence requirements when investing in emerging markets. Africa is no exception and is often perceived as a higher-risk region, even among seasoned EM investors. As a result, ensuring clarity and transparency from the outset of any project is essential.

7. Where do companies most often fall short when presenting themselves to Gulf investors – is it a question of messaging, transparency, alignment with investor priorities, or execution?

Given the sophisticated nature of Gulf capital, there is a high level of selectivity when it comes to choosing investment projects. Foreign companies need to be intentional and clear in presenting themselves to Gulf investors. Beyond the value they create, they will need to explain what advantages they are bringing to the Gulf and highlight potential alignment with regional policy frameworks.

8. How do you see the Gulf–Africa investment corridor evolving over the next five years, and what should businesses be doing now to position themselves credibly and competitively?

While some parts of the world are becoming more introverted, others need to increase interaction with peers to address issues like climate or energy shifts. The Gulf and Africa belong to the second group, translating into a natural tendency towards more geo-economic interaction in the coming years. Foreign investors will not only encounter annual population growth rates of more than 2% in sub-Saharan Africa but also an expanding middle class whose purchasing power is rising over time.

9. What implications do you think the closure of the strait of Hormuz and UAE’s departure from OPEC could have on Gulf-Africa relations?

If anything, the strait closure should emphasize the need for further Gulf cooperation with east African nations in order to also secure free passage for ships and trade through the Red Sea. UAE’s departure from OPEC probably won’t have any direct effect on Gulf-Africa relations, given each GCC country has pursued its own trade and investment policies with Africa. UAE is already the GCC’s largest trade and investment partner for Africa.

10. If you had one piece of advice for CEOs engaging with Gulf investors for the first time, what would it be?

As you will be aware, you are dealing with highly experienced investors who need to be presented with a clear rationale to deploy their capital abroad rather than at home. The best approach would probably be to explore projects that are to-the-point, forward-looking and, above all, that can be mutually beneficial.